The new long-term energy plan for Hawaii is getting better reviews than its two predecessors, but it won’t be the last word on how the state will get to 100% renewables by 2045.

Stakeholders have raised two main concerns about the 1,800-page Power Supply Improvement Plan (PSIP), filed with regulators last month.

First, to reach the 100% renewables mandate may come at an unaffordable price for customers of the Hawaiian Electric Companies, the state’s dominant electricity providers.

Second, three key stakeholder groups raised longstanding concerns about HECO’s vision for distributed resources and the evolution of its business model.

HECO’s first PSIP was filed in 2014, and roundly rejected by regulators in Nov. 2015. In their order and a subsequent white paper, Hawaii Public Utilities Commission (PUC) told the utility to “implement the vision for the ‘electric utility of the future,’” including a “a customer focused business strategy” instead of “unrelated capital projects without strategic focus.”

HECO then filed another plan last year that called for imports of liquefied natural gas (LNG) to help the state bridge the gap to 100% renewables. But it was contingent on PUC approval of HECO’s merger with Florida-based NextEra Energy, and the utility withdrew the plan when the acquisition was rejected by regulators.

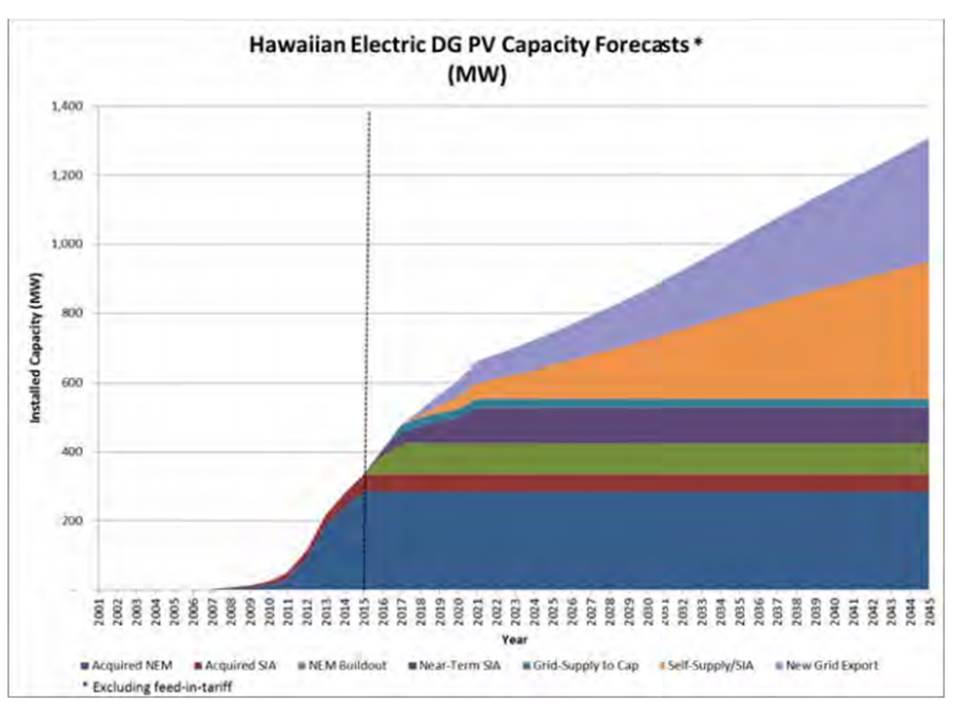

The basis of the new PSIP is a five-year action plan that would take the state to 48% renewables by 2020 and to 72% renewables by 2030. By 2021, Hawaii would have 326 MW of distributed photovoltaic solar generation (DG-PV), 360 MW of utility-scale PV, 157 MW of utility-scale wind energy, 114.7 MW of demand response (DR), and 31 MW of feed-in tariff-funded renewables.

But potential generation mixes that would get Hawaii to 100% renewables by 2045 could cost Oahu utility customers an estimated $26.5 billion by 2045. Costs to Maui and Hawaii Island utility customers add $10 billion more.

“It is not clear the over-50% increase in the utility revenue requirement through 2021 is the customer-focused, strategic investment required by [the PUC white paper],’” Earthjustice Attorney Isaac Moriwake, representing key stakeholder Sierra Club, told Utility Dive.

The emphasis on liquefied natural gas (LNG) has changed to an emphasis on wind, solar, and energy storage and that is “a definite improvement,” Moriwake said. “But HECO treats distributed energy resources [DER] as something that happens to the utility and fails to envision a new system.”

HECO Sr. VP for Planning and Technology Colton Ching insisted this PSIP does meet the two fundamental directives from the PUC white paper.

First, to meet the state’s 100% renewable portfolio standard (RPS), HECO will become “the utility of the future” and build “a grid of the future," Ching said.

Second, to fund this change, HECO will displace costly oil-fueled generation with low cost renewable energy. “The [white paper] envisioned that tradeoff,” Ching said. “It is the best way to get to 100% renewables.”

“Substantial investment in the grid is necessary to interconnect the new renewables and to integrate the DER customers want. That is the strategic focus,” he added. “That grid will be critical when there are 3,008 MW of DG on it in 2045 across all five islands.”

The preliminary reaction from Hawaii Division of Consumer Advocacy Executive Director Dean Nishina is that the refocused plan is “more actionable” and “appears to have better considered an expanded portfolio of resources.”

It is, however, not yet clear this is “the most cost effective plan,” he added.

The nonprofit Blue Planet Foundation was one of the earliest stakeholders to push for the 100% renewables standard. Policy Director Richard Wallsgrove sees “a lot of good things” in the five-year plan but said “some of the hard questions may be pushed off.”

Planning in five year phases is reasonable for HECO but “things are changing faster in the energy sector than our imaginations can keep up with,” Wallsgrove said. Biofuels may offer an emissions-neutral alternative in the 2040s, but at an increased cost. “This plan modernizes thermal generation but does it make sense to plan on burning stuff in 30 years? Why not include visionary options for the longer term?”

What of the cost?

HECO developed the basic action plan and alternative long term scenarios with consultant Environmental + Energy Economics (E3), using E3’s RESOLVE modeling program.

Each alternative scenario offers a resource mix out to 2045 that economic circumstances and technological advances could make the best choice.

HECO’s basic long term scenario is labeled the “Post-April PSIP Plan.” Alternatives include a basic “E3 Plan,” an “E3 Plan with LNG,” an “E3 Plan with Grid Modernization,” and an “E3 Plan with Grid Modernization and LNG.” Each includes variations specific to Oahu, Hawaii Island, or Maui.

Each makes “concerted efforts to minimize the financial impact on customers,” the PSIP reports.

Nevertheless, Consumer Advocacy’s Nishina is concerned about the size of the capital investment and “the possible cost impact on customers.”

Presently, Hawaii’s electricity rate and the price of the diesel oil used to generate about 80% of its power are low. Yet “customers are complaining about the rates and total bills,” Nishina said. “While the proposed investments may reduce the exposure to the volatility of oil prices, such an investment will likely make electricity too expensive for many customers.”

The PSIP acknowledges these impacts. The costs of grid modernization, ending fossil fuel use, and “aggressive deployment of low-cost renewables,” it reports, “will move customer bills higher in the near term.”

The net present value of the revenue requirements in the 2045 scenarios range from $24.9 billion to $26.5 billion. But as the state reaches its goal, the PSIP argues, “the aggressive pursuit of low-cost renewables will cause customer bills to be flat or slightly declining on a real-dollar basis.”

HECO calculations show the revenue requirements result in annual rate increases of roughly 2.5% to 3.5%, with 2% attributed to inflation, over 30 years, according to Ching.

“The five-year action plan was not based on any single long term scenario because there is too much uncertainty,” HECO’s Ching said. Though different in the long term, the scenarios were “very similar, and in some cases identical, in the near term and that assured us the five-year action plan fits well with however things evolve.”

Blue Planet’s Wallsgrove sees this as reasonable planning and has read other analyses verifying HECO’s argument about the capital expense. The approximately $26 billion in fuel cost savings through 2045 would balance the $26 billion revenue requirement, he said. “That suggests there will not be a radical increase in ratepayer costs.”

Using LNG longer extends fuel costs later into the transition but does not create “big savings,” Wallsgrove said.

Shifting that money into the capital expenses column does, however, provide the utility with a rate of return for the investment instead of a pass-through expense. “It raises questions about what the plan means for the utility bottom line and the utility revenue model,” Wallsgrove said. “Those questions should be answered by the PUC with stakeholder input.”

That is the point, Moriwake insisted. “HECO’s business is at the center of this plan. The increased revenue requirement will substantially and directly benefit the utility business and its shareholders.”

It could be the best plan a regulated utility like HECO could offer, he said. “But is there a more comprehensive plan that would get to 100% renewables with totally different or less costly resources? That is what we don’t know.”

HECO's DER vision — or lack thereof

There is little doubt of the plan’s commitment to renewables. Its first principle is “renewable energy is the first option.” And it leaves no question about the utility’s recognition of DER.

Because “advances in technology continue to drive costs down,” it reports, “we assume high levels of DER penetration and will work to enable the integration of right-sized and right-priced systems.”

The grid modernization “empowers customer choice where distributed energy resources—solar PV, energy storage batteries, electric vehicles, and demand response resources—can operate at every home.”

The 3,008 MW of DG PV forecast for 2045 “assumes all single-family residential homes and 20% to 25% of commercial customers produce the same amount of PV energy as they consume,” the plan adds.

Ching noted that the cost of utility-scale renewables will not add to HECO’s rate base. “We expect to contract for the utility-scale generation from independent power producers,” he said.

“We are preparing for the high DG PV scenario and not simply the market projection,” he added. "The capital expenditure in the PSIP is for the upgrades to HECO’s aging transmission and distribution systems that will enable the high penetration of variable utility-scale renewables and DG PV."

The newest concern about the high DG PV scenario is reflected in just-filed proposals to the PUC by the Distributed Energy Resources Council of Hawaii (DERC), the Energy Freedom Coalition of America (EFCA), and The Alliance for Solar Choice (TASC). All three groups represent significant numbers of DER providers.

Data behind the filings suggests there may be a “material mistake” in the plan, said TASC Spokesperson Robert Harris. It is “not malicious” but, if the groups are correct, the mistake could have“major ramifications.”

The PSIP may “significantly” underestimate the amount of behind-the-meter (BTM) battery storage that will accompany the installation of DG PV, Harris said.

Because of a gathering set of regulatory and market factors, the filings call for terminating the export of solar to Hawaii’s grid between 9AM and 4PM. One of factors was the result of the PUC’s decision to terminate retail rate net energy metering (NEM).

The decision was due to the challenge to HECO’s distribution system from the state’s abundant DG PV. To manage over-generation, the “CGS tariff” that replaced NEM allowed only reduced remuneration for exported solar-generated electricity during non-peak demand periods. And it is almost fully subscribed.

New DG PV installations will now earn little value for exported power because HECO’s resources are more than adequate to meet system needs during the high solar generation off-peak hours. Going forward, DG PV's chief value to Hawaii’s solar owners will be in replacing non-peak demand high-priced electricity and even higher-priced peak demand electricity.

The increasingly affordable electricity supplied by DG PV makes this practical. The falling cost of battery storage enhances the value proposition, especially in the absence of remuneration for exported generation.

“The key point is that it is unlikely any more solar without storage is going to be coming on,” Harris said. “That would potentially bring hundreds more MW of storage online sooner as a grid resource. It is a great thing but it changes all the assumptions in the PSIP.”

The filings do not identify how big HECO’s potential miscalculation is but Harris believes it will significantly diminish system load and alter PSIP assumptions about curtailment.

Ching believes HECO’s planning is adequate to this concern. “We do account for a very high amount of distributed storage and distributed storage plus PV, as incorporated in our sales and peak forecast,” Ching responded. The utility recognizes it as “flexible load” that can expand its DR portfolio as well.

There are also over 150 MW of DG-PV still to be added that, by an accounting anomaly, remain eligible for the export tariff, Ching added.

Finally, he said, a successor tariff for exported power is being developed “very quickly” by stakeholders and Hawaii utilities in an ongoing regulatory proceeding. “We've assumed that CGS successor in our DG-PV forecast.”

Consumer Advocacy’s Nishina said the best assessment of the plan may not be possible until the current rate restructuring is complete. “Until the rate structure and rates are properly updated, customers will not be given the appropriate pricing signals and inefficient investment decisions will continue to be made.”

On the larger point of whether the PSIP represents “customer-centered strategic planning,” Ching expanded his argument. “We are now building a distribution grid that proactively builds intelligence, creates a communications system, and enables a much higher level of DER.”

The PSIP calls this a “paradigm shift” and promises an “integrated grid” that “will enable DER to provide the services that are lost with the deactivation of traditional centralized conventional generation.”

The plan is for a modern plug-and-play grid that incorporates “advanced metering, a demand response management system, and an advanced distribution management system,” the PSIP promises. “We envision an advanced distribution system where customers can plug their distributed resources into the grid.”

The plan also describes utility thinking about rate designs that send price signals about EV charging so they can be used “as a load and as demand response to help with the integration of renewables,” Ching said.

The state of the technology, economics, and customer adoption for things like EVs and distributed storage are changing rapidly, Ching added. The PSIP’s commitment to continuous planning recognizes that “no one knows today what will happen in the long term.”

Blue Planet’s Wallsgrove sees in PSIP language potential new directions for HECO’s business model.

“It is somewhat visionary about how electrifying transportation will be part of planning load and planning the generation to meet it,” he said. “That is going out and attacking the market rather than just waiting for it.”

HECO also describes revenue opportunities outside its core business that will increase the customer value proposition and acknowledges this change as necessary to remain competitive, he pointed out. Plans for EVs could “accelerate the implementation of renewable energy and storage options, while driving down the total cost of energy for all customers."

The PSIP’s forecast, however, is based on historical trends and may significantly underestimate growth, Wallsgrove said. This tendency extends to DG-PV and energy efficiency and, in this way, seems to fail to meet the PUC directive to “optimize” DER, he added.

Moriwake supported his concern by arguing the PSIP still fails to fully address the PUC’s objections to previous utility long-term plans for DER. “That is a symptom of utility-centric planning,” he said.

Because of Hawaii’s unprecedentedly high penetration of DG PV, “HECO is a national leader at integrating rooftop solar into the traditional utility grid," Moriwake said. “But the PUC directed it to find a new model that optimizes DER and makes it part of a new and transformed system instead of cramming it into the traditional utility business.”

The remedy, Moriwake has come to believe, “is an independent third party to do the planning. This is now bigger than HECO.”

Appendix Q and the customer exit mystery

Appendix Q, at the end of the document, is titled Customer Exit Economic Analysis. It is one extraordinary sentence:

“Pages Q-2 through Q-4 contain confidential and/or proprietary information, and are designated as ‘restricted information’ to be provided only to the Commission and the Consumer Advocate, and not to be distributed to any other party or participant to this proceeding or its representatives.”

HECO’s Ching called the appendix “a roadmap or instruction sheet for competitors to take our customers off-grid.”

To date, a significant minority of customers have chosen load defection, or the use of their own DG to supply some of their power. When they do so, the utility is forced to impose system costs on other customers.

As the costs and effectiveness of DG PV, BTM battery storage, and energy efficiency measures become increasingly affordable, customers may choose grid defection, which is leaving the utility entirely.

Appendix Q apparently addresses “the $26 billion dollar question,” Moriwake said. “Will escalating spending drive customers to exit the grid?”

Ching said HECO “will not share the details of the analysis with the parties in the docket because of its competitive nature.”

Former PUC Chair Mina Morita, who led the commission that produced the PUC white paper guidance, called for a more public release of the information. She is concerned that market factors and state incentives will drive significant defection.

“All stakeholders, especially policymakers, need to understand whether, if prompted by misguided public policy, the $26 billion in revenue requirements in the PSIP might end in stranded assets and with dire consequences for customers remaining on the grid,” she told Utility Dive.

Outside the commission, only the consumer advocate’s office now knows. It has pushed for more transparency, but shares the utility’s concern with revealing information that could drive defection and higher prices for remaining customers, Nishina said. The solution, he added, are new tariffs with price signals that eliminate the problem.

Ching staunchly defended the utility’s decision to keep the information confidential. “We absolutely are in a competitive environment,” he said. “There is nothing our competitors cannot find out but we just don’t think we need to give them an instruction sheet.”

Appendix Q describes the type of customer that might be more economically benefited by going off-grid and the most competitive combination of DG PV and battery system sizes, Ching said. He declined to identify specific competitors.

TASC’s Harris, who represents the solar and DER providers who many see as the utility’s competitors, said customer exit should be discussed publicly. “Some of the assumptions may be proprietary but discussing the end result is important.”

Solar and DER providers should not be the utility’s concern, he argued “It is their own customers who are making the decision to leave the grid. They are competitors. The real question is whether the utility can provide the services customers want at a price they are willing to pay.”

Ching acknowledged that the best way to prevent defection is for the utility to keep electricity rates as low as possible and create added value for customers’ grid-connected DER. But he also expressed concern about the potential of customers turning to diesel generators for back up and worsening the state’s emissions problem.

Moriwake dismissed this. “Customer-owned solar plus battery systems are already cheaper than utility power and the PSIP assumes continued high customer adoption."

And, he added, "a 50% rate increase over the next few years could drive a lot more customer exit and show HECO is moving against the tide of history.”