With wholesale power prices low and federal power regulations in limbo, choosing the right generation investments has never been trickier — or riskier — for utilities and independent power producers.

A new study could help, simplifying the decision into clear, cold numbers.

In 2016, natural gas provided 42% of U.S. power capacity and led all resources with 34% of total generation. Solar, however, led in capacity added with more than 14,700 MW, accounting for 39% of the U.S. total. And wind energy accounted for 30% of the capacity installed since 2012. In 2016 its total installed capacity reached above 82 GW in the U.S.

In deciding between renewables and natural gas generation, a utility wants the most economic and reliable choice. A new Lawrence Berkeley National Laboratory (LBNL) study offers a new way to compare them, showing that renewable resources have added value as hedges against natural gas price volatility.

The study’s “statistical concept” quantifies the probable risks of each resource and factors them into a levelized cost of energy (LCOE) comparison, according to LBNL Researcher Mark Bolinger, co-author of “Using Probability of Exceedance to Compare the Resource Risk of Renewable and Gas-Fired Generation.”

Probability of exceedance is commonly used by IPPs and utility planners “to characterize the uncertainty around annual energy production for wind and solar projects,” the paper reports. It “can also be applied to natural gas price projections.”

Statisticians label the mid-range case “P50,” but calculate a probability for all possibilities from P1 to P99. The LBNL study quantifies the risk at each P-level of expected renewables output levels and natural gas prices.

“In general, higher-than-expected gas prices appear to be riskier to ratepayers than lower-than-expected wind or solar output," Bolinger said.

Utilities contracted for or owned 55% of 2016’s installed wind capacity and utility interest has continued into Q1 2017, according to the American Wind Energy Association. Utilities are also expected to contract for two-thirds of the 13.2 GW of solar forecasted to be added this year, according to the U.S. Solar Market Insight 2016 Year In Review.

Even so, utility planners may be underestimating the hedge value of these renewable resources. Utility Dive's survey of more than 600 sector professionals revealed only 7% see natural gas price volatility as the primary reason to invest in renewables.

If the LBNL methodology gains traction, it could have a significant impact on how utilities plan their generation portfolios.

Comparing risks

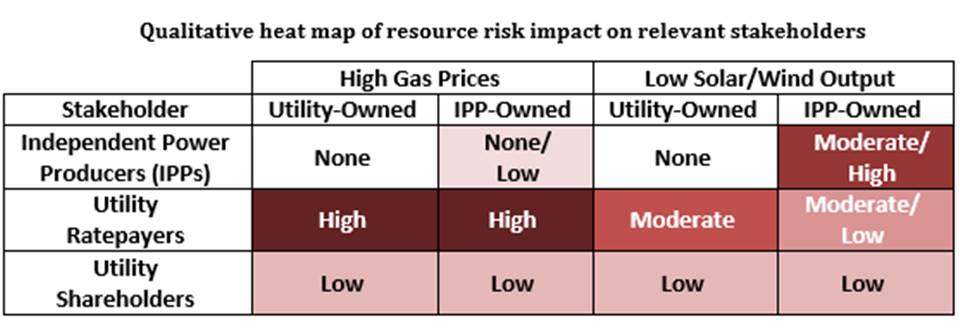

Of the many risks that come with investments in new generation, resource risk is the one that most clearly distinguishes renewables from natural gas, LBNL reports.

For renewables, the risk is “the quantity of wind and insolation will be less than expected.” For natural gas, the risk is “natural gas will cost more than expected.”

Resource risk, and especially natural gas price volatility, “falls disproportionately on utility ratepayers, who are typically not well-equipped to manage this risk,” LBNL reports. Utility shareholders and IPPs are significantly less affected.

“Utilities, regulators, and policymakers have a responsibility to consider this risk because they are charged with looking out for the interest of ratepayers,” Bolinger said.

When gas prices are higher than expected, ratepayers are typically the ones who suffer, LBNL reports.

Michael Goggin, director of research at the American Wind Energy Association (AWEA), said the study’s concepts “could easily be adopted” for utility integrated resource planning (IRP).

“Planners do scenario analysis and use high, low, and a mid-range gas prices, but we have seen higher than high case and lower than low case prices,” Goggin said. “There is also a tendency to expect the mid-range case, though the other cases are very real.”

Probability of exceedance concepts allow “a probabilistic range of projections for not only wind and solar capacity factors, but also natural gas prices,” the paper reports.

If the solar or wind resource at a project site is less than anticipated, the renewable project’s output will be lowered. That will lead to a higher than expected LCOE because “there is less wind or solar generation over which to spread up-front capital costs,” Bolinger said.

The LCOE for a natural gas plant will be higher if the natural gas market price is higher than expected, he added. The LCOE allows comparison of “two different manifestations of resource risk that would not otherwise be directly comparable.”

For renewables, P-levels between P1 and P49 indicate below-expected output, lower-than-expected capacity factors, and, therefore, higher than expected LCOEs. P51 and higher levels indicate better-than-expected outputs that lead to lower-than-expected LCOEs.

For natural gas generation, P-levels between P1 and P49 indicate lower-than-expected market prices that lead to lower-than-expected LCOEs. P51 and higher levels indicate higher-than-expected market prices and higher-than-expected LCOEs.

The study specifically compares LCOEs of renewables affected by lower-than-expected outputs and LCOEs of natural gas generation affected by higher-than-expected market prices, Bolinger said.

“It shows which deviation from the expected, at any given level of deviation and over any time horizon, will have a bigger impact on the cost of electricity in dollars per MWh,” he said.

Resources are most often compared at the P50 mid-range level, when natural gas generation “is competitive with, or cheaper than, wind and solar power,” the study reports. But “worse-than-expected” P25 or P1 outcomes “often reach the opposite conclusion: that wind and solar are cheaper than gas-fired generation.”

An example: Wind without the production tax credit is not cost-competitive with natural gas generation in the expected P50 case. But, in worse-than-expected outcomes of P49 and below, where natural gas market prices are high and/or wind output is low, wind is competitive. And it gets more competitive over time.

With worse-than-expected gas prices and capacity factors, renewables end up being cheaper than gas plants, LBNL found.

Another example: A utility-scale PV solar project with the investment tax credit is similarly uncompetitive unless natural gas market prices are high and/or solar output is low. Though the time frame is longer, solar in the P49 and below cases eventually becomes competitive.

Solar also fares better than gas under worse-than-expected market conditions, albiet over a longer timeframe than wind resources.

Where the curves cross, the renewables take on “hedge value” that increases as the buyer's “risk aversion” increases and/or as the “time horizon” lengthens, the study reports.

The timeline is important, Bolinger said. Yearly variations of renewables show increasing certainty "over a 10-year or 20-year period." Natural gas prices are "somewhat predictable over the next month, less so over the next year, and almost impossible to predict over 10 years or 20 years."

Every study is limited by its assumptions, Bolinger added. This study assumed a level of natural gas market price uncertainty based on the post-2008 period, when the price was relatively stable compared to earlier periods.

“The most conservative assumption we could make was that this recent period of relative stability in gas prices, due to shale gas, is going to continue," he said.

The difference in risk between natural gas and renewables “would be much wider if shale gas reserves are smaller and the more limited supply drives market prices higher,” Bolinger said. In that case, wind and solar would have even better hedge value. “Because natural gas prices are already at historical lows, there is less risk they will fall significantly.”

These probability assumptions and calculations provide a basis for choosing between a higher-than-expected gas price scenario and a lower-than-expected wind or solar resource scenario with the same probability, the study reports. “The impact of the high gas price scenario may be more harmful to ratepayers than the impact of the low wind/solar resource scenario.”

The LBNL researchers argue that the framework’s “probabilistic nature” is a key advantage of the the method. Other advantages are that it recognizes wind and solar have resource risk, the methodology requires relatively simple inputs, and it can be used for any level of risk aversion over any time horizon.

Its key disadvantage is that resource portfolio decisions are not made, and should not be made, “on LCOE alone,” LBNL concludes.

Perspectives on the LBNL paper

Charlie Reidl, Executive Director of the Center for Liquefied Natural Gas (LNG), does not expect natural gas price volatility. Even with LNG exports to meet a growing global demand, “the price impact is negligible.”

The export of as much as 20 billion cubic feet per day of natural gas would not put price pressure on the estimated 325 trillion cubic feet of “proven U.S. reserves,” he said.

Other authorities argue U.S. reserves are being depleted too rapidly to keep up with demand. The disagreement underscores the importance of a method like LBNL's that quantifies the risk and uncertainty.

Joseph Desmond, vice president with utility-scale solar builder BrightSource Energy, called the LBNL paper “an important contribution.”

There are a variety of other methods to compare the risks of renewables and gas, but none, on its own, “has been entirely satisfactory,” he said. This method makes it “easier to understand and value” the hedge value renewables offer over time.

The LBNL paper reports on a recent New Mexico regulatory filing by Xcel Energy subsidiary Southwestern Public Service (SPS). A proposed procurement of 1,230 MW of new wind, the filing reports, would displace 22 billion cubic feet of natural gas at a "lowest case price" of $2.40 per million British thermal units.

“The $2.40 comes from the wind contract price,” Bolinger said. “This example was included to demonstrate that the comparison we are making is not just academic. Utility planners take hedge value into account in making decisions on wind and solar procurements.”

The proposed SPS wind procurement is “grounded in economics, not on an energy policy of promoting any particular fuel type,” President David T. Hudson testified to New Mexico regulators. “The stable price of these resources provides protection against future volatility in natural gas markets.”

The SPS wind’s LCOE “is $18.97 over 25 years.” Hudson reported. SPS’s projected 2017 cost of natural gas generation is $33.03/MWh and the projected 2020 price is $29.70/MWh, he added.

From a long-term perspective, the wind acquisition looks “even more impressive,” Hudson added. The cost of the wind project is estimated to be “approximately $1.63 billion” and it is expected to deliver “$2.8 billion in total customer savings over 30 years.”

AWEA’s Goggin said probability exceedance “is one of several tools used by the financial industry to quantify and manage risk and understand ways to reduce it.” The importance of the LBNL tool is that it results in “transparent and quantifiable values."

The study shows that fixed-price utility-scale renewables provide “insurance that protects customers from a very real fuel price risk," Goggin said. The several periods in recent decades of “extreme natural gas price volatility” make it reasonable to expect that it could happen again.

“Nobody can predict future prices, he said. “But even with abundant shale reserves, greater reliance on natural gas for electricity, for heating, for industrial processes, and as an exported commodity could lead to even price higher volatility.”

Corporate buyers are contracting for renewables because high power bills expose them to market volatility and they see bottom line value in a long term fixed price, Goggin said. Regulators are approving utility purchases of renewables for the same reason. “They see it is in the interest of utility customers to keep prices down and electricity delivery reliable.”