New forecasts say the high penetrations of renewables coming onto the U.S. power system by 2030 could accelerate recent isolated instances of negative and spiking prices in wholesale markets.

Research from Lawrence Berkeley National Laboratory (LBNL) shows higher renewables penetrations could cause these supply-demand imbalances more frequently, imposing instability in power markets.

If this growth pattern continues, as many expect it will, grid operators and renewables developers will need to act to neutralize price volatility by making the electric power system more flexible, the LBNL researchers reported.

As more solar and wind power comes online, renewables penetrations are reaching unprecedented levels in some places. On March 31, wind momentarily reached a North American record of over 62% of Southwest Power Pool (SPP) generation. On April 28, renewables met 72.7% of demand for the California Independent System Operator (CAISO).

While the numbers are much smaller nationally, broader indications show unremitting growth of variable renewable energy (VRE). Grid operators are implementing a variety of steps to integrate that new capacity while minimizing adverse impacts on the system.

The threat of growth

Many long-lasting decisions about the power system "assume a business-as-usual future with low shares of VRE." But a "high VRE future" can lead to "profound changes in wholesale electricity price patterns," such as extreme price drops and spikes, according to LBNL's report.

When generation oversupply forces project owners to bid into markets at their own cost, just to keep generating, it can cause power prices to plunge below $0/MWh. Additionally, power prices spike to untenable highs when demand peaks in supply-constrained localized areas.

In May, renewables served an average of almost 36.1% of the CAISO load, up from 2016's 21%, with solar providing about 52% of the renewable generation and wind about 29%. Wind was 20.2% of total SPP system capacity at the end of 2017, up from 2016's 19%. The 2017 wind generation capacity on the Electric Reliability Council of Texas system was 19.6%, up from 2016's 13%. Even New York's tiny 4% was a 25% increase on 2016's 3%.

Of the total 24,614 MW of new U.S, generating capacity in 2017, wind's 6,881 MW accounted for 27.9%, and solar's 4,853 MW added another 19.7%, according to Federal Energy Regulatory Commission data. That made VRE the single biggest source of new U.S. generation capacity in 2017.

Threat or opportunity?

The LBNL researchers modeled four 2030 VRE scenarios. One was a business-as-usual scenario with today's VRE penetrations, and one was a "balanced" 20% wind-20% solar scenario. The other two scenarios had either 30% solar and 10% wind or 30% wind and 10% solar.

VRE penetrations of 40% or more would drive down average annual hourly wholesale energy prices "by $5/MWh to $16/MWh depending on the region and mix of wind and solar," LBNL reported. The price impact is much greater at times of wind or solar overgeneration, the modeling found.

Ten years ago, U.S. National Renewable Energy Laboratory (NREL) researchers first saw rising renewables penetrations. Like today's researchers, they were concerned. That concern led them to discover new system operations that have kept then-predicted price volatility in check and transformed the threat into today's renewables boom. It can happen again, LBNL Research Scientist Ryan Wiser told Utility Dive.

The LBNL findings

The research shows high VRE penetrations can make future price patterns "meaningfully different," said LBNL's Wiser, lead author of the new report.

There could be "a general decrease in average annual hourly wholesale energy prices" and "increased price volatility and frequency of very low-priced hours."

Current penetrations of VRE have led to very little of the recent price volatility, Wiser told Utility Dive.

Previous LBNL work showed "about 90% to 95% of the explanatory factors for the average annual wholesale price decline of about $0.04/kWh between 2008 and 2016 was driven by the decline in natural gas prices," he said.

There was also "no observable widespread impact of VRE on thermal plant retirements," he added. Instead, "plant characteristics" forced the closures seen over the last decade.

There was, however, a "significant increase" in negative wholesale pricing and curtailments between 2015 and 2017, Wiser said. "This is quite clearly correlated with both the growth of wind and solar, and the location of that growth."

Curtailment occurs when grid operators shut down renewables generation in response to negative prices and oversupply on their systems.

"Some plants are experiencing negative wholesale prices as much as 25% of the year's hours."

Ryan Wiser

Research scientist, LBNL

Curtailment has increased particularly in California with the growth of solar and in the U.S. Midwest, with the growth of wind, Wiser said. "Some plants are experiencing negative wholesale prices as much as 25% of the year's hours."

The new LBNL work shows high VRE scenarios can lead to "modest retirement" of between 4% to 16% of older fossil fuel plants. A $0.21/MWh to $0.87/MWh average price reduction for each 1% of VRE "primarily displaces coal and natural gas generation."

The lower prices are largely taken by "inflexible generators," especially nuclear, solar and wind, LBNL found. Where higher VRE leads to less overgeneration, the price drop is lower. Where there is overgeneration, the price drop is "a pronounced cliff, featuring a dramatic increase in hours with very low prices."

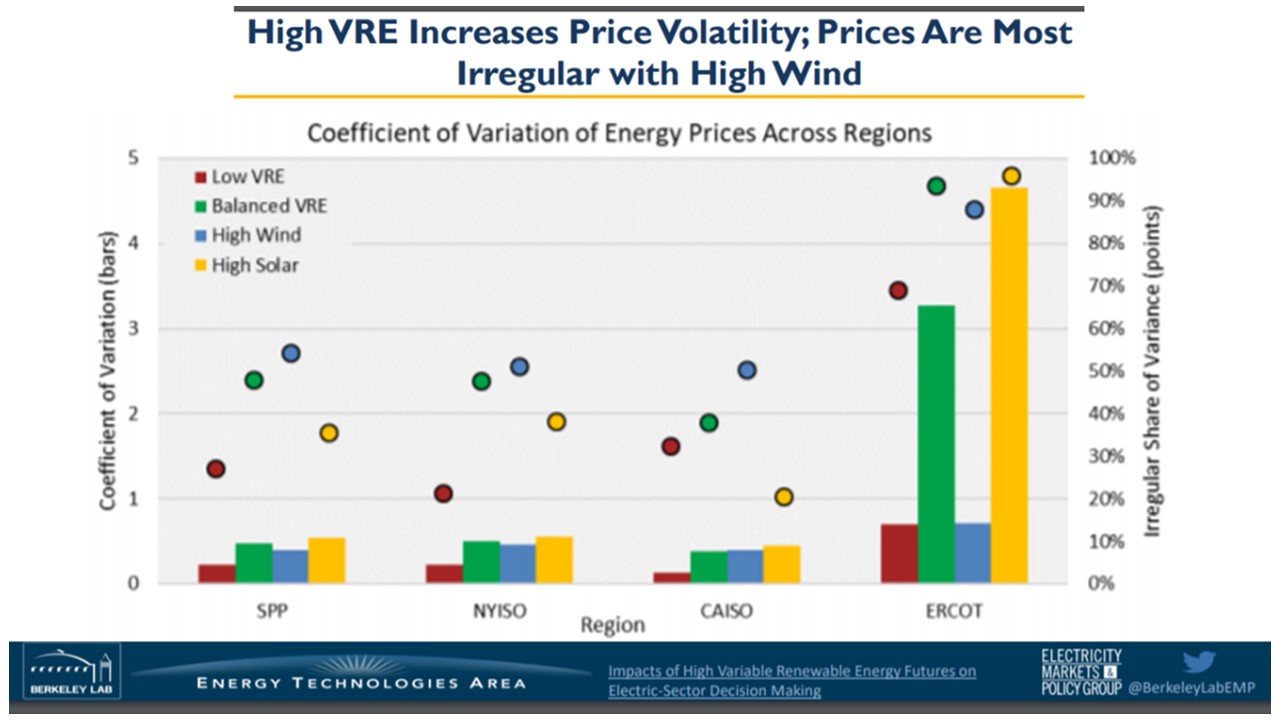

Total price volatility was greatest in LBNL's high solar scenarios, but the greatest irregularity in prices was in the high wind scenarios. In all high VRE scenarios, the system peak demand periods remain, but they tend to be pushed to later in the evening, especially in the high solar scenarios.

Existing solutions

Negative pricing and curtailment have historically been found where transmission constraints prevented alleviation of local overgeneration, Wiser said.

A system with more transmission capacity or operating procedures "friendlier" to high VRE penetrations could avoid the consequences described by LBNL's modeling, he said. Another set of possible solutions would be to make VRE friendlier to systems, he added.

"System-friendly renewables bring technical and siting solutions to increase their market value," Wiser said. "More renewables-friendly systems have more transmission and more operational flexibility. The bottom line is that there are ways of managing or mitigating the market value depressing effect and the wholesale market price decline of high VRE scenarios."

Solar and the grid

A solar-friendly wholesale electricity system would have smooth, multi-hour time ramps rather than the short, steep demand spikes caused by midday solar overgeneration, LBNL research scientist and paper co-author Andrew Mills emailed Utility Dive. It would also have large balancing areas, or collaboration between balancing areas, to smooth momentary production fluctuations.

Flexible generation that can be turned off and on multiple times a day could reduce overgeneration, he added. Well-crafted rate designs would give customers price signals that align demand with supply.

System-friendly PV could do some of the same things, Mills said. Utility-scale projects could be sited and located strategically to prevent overloading circuits, protect against momentary output disruptions and produce when demand is higher, he said. Utility-scale projects can provide more services to the system operators if they are equipped with smart inverters, active power controls and on-site storage, he added.

These are the kinds of strategies CAISO is working toward, according to Senior Public Information Officer Steven Greenlee. At the most basic level, system-friendly resources respond to negative prices by reducing output, he emailed Utility Dive.

"Negative prices and oversupply challenge the energy community," he said. "An October 2017 report from NREL, CAISO and project developer First Solar demonstrated the market can use the newest technologies to improve the efficiencies and services resources deliver."

In addition, CAISO is working with the California Public Utilities Commission on time-of-use rates that will provide the kind of price signals Mills described. Other CAISO initiatives are aimed at lowering barriers to the integration and market participation of DER and energy storage. Both will make the system more flexible, Greenlee added.

"The battery storage option is clearly a big winner for solar," Wiser agreed. "All that is necessary is to shift the solar a few hours into the evening. It is harder to see the value proposition for battery storage co-located with wind because wind needs longer-term storage to be valuable. Transmission is a more logical and less costly solution for wind."

Wind and the grid

Turbines with taller towers, larger rotors, and advanced capabilities can make wind system-friendly by bringing the levelized cost down and providing system balancing, according to an October 2017 International Energy Agency study.

Other system-friendly things wind developers can do include optimizing siting and expanding siting diversity, LBNL reported. Integrating storage and other power electronics can allow a project to provide grid services, LBNL also reported.

The system can be friendlier to wind if it has more generation flexibility and more available transmission capacity, LBNL added. It can offer more flexibility with advanced operational and market practices.

SPP ran headlong into the need for system-friendly wind in 2017, Market Monitoring Unit Executive Director Keith Collins told Utility Dive. "The incidence of negative prices doubled in 2017 to about 7% of real-time intervals, up from about 3.5% of intervals in 2016," he said. "They were concentrated in the overnight hours, when almost 15% of intervals had negative pricing."

SPP's 2017 State of the SPP Market report highlights two key opportunities to enhance the flexibility of the system by changes in the way wind generators participate in the SPP market, he said.

One change is to require non-dispatchable renewables, and especially wind, to become dispatchable through a system-friendly change in reporting, Collins said.

"Dispatchable resources provide a forecasted level of production and a price at which they will curtail output," Collins said. "Non-dispatchable wind resources do not provide a price. This creates market inefficiencies that contribute to negative pricing as well as operational issues, Collins said.

SPP's report also describes a concern with under-scheduling by wind producers in the Day-Ahead market, he added. It is the main reason there is almost twice the negative prices in the Real-Time market.

Finally, SPP could make its system more wind-friendly by developing a ramping product "to deal with unexpected and expected ramps in demand, Collins said. "There is now ramping-related scarcity pricing. A ramping product would likely dampen some of that pricing volatility."

Looking back and ahead

NREL Principal Analyst Paul Denholm led some of the earliest work on the challenges associated with renewables overgeneration in 2008. His 2015 NREL work identified early system-friendly and renewables-friendly strategies aimed at adding power system flexibility.

But his work is just beginning, Denholm recently told Utility Dive. Policymakers are now aiming for 50% renewables and researchers are thinking about 100% renewables. More system flexibility will be vital because "fluctuations are going to get worse," he said. But "we shouldn't confuse a challenge with an insurmountable problem," he added. "It simply requires a new way of operating the power system."